The Misplaced Default Narrative

Headlines warning of U.S. sovereign default have resurfaced alongside elevated Treasury yields. Social media amplifies charts showing trillions in maturing debt, while commentators question America's ability to service its obligations. Yet this narrative fundamentally misunderstands how sovereign currency issuers operate—and what Treasury yields actually communicate to market participants.

The United States government issues debt denominated in a currency it controls. This structural reality distinguishes sovereign debt from corporate or municipal obligations in a fundamental way: the federal government maintains the capacity to service its debts through currency issuance. The relevant risk is not whether America pays its bills, but rather the inflationary consequences of fiscal and monetary policy choices.

When Treasury yields rise, sophisticated market participants understand the signal: expectations about future inflation, concerns about fiscal policy direction, and demands for term premium compensation. These are legitimate economic considerations. Sovereign credit risk, in the traditional sense, is not among them.

Perception Versus Market Reality

The distinction between inflation risk and credit risk carries profound implications for interpreting market signals. Current yields above 5% on certain Treasury maturities reflect several factors: concerns about persistent inflation, uncertainty surrounding fiscal policy, and expanded term premiums demanded by investors for duration exposure.

Market anxiety centers on policy trajectory—spending plans, tariff implications, and their potential inflationary effects. These concerns are economically valid and appropriately reflected in yield levels. However, they represent fundamentally different risks than questions about debt service capacity.

Observing institutional behavior provides clarity. Insurance companies, pension funds, and sovereign wealth managers continue allocating to Treasuries not from obligation alone, but from rigorous assessment of alternatives. When institutions managing hundreds of billions consistently choose Treasury securities, they signal confidence in the asset class that transcends headline concerns.

Notable institutional investors maintain substantial Treasury allocations, with some holding over $300 billion in short-term government securities. This behavior reflects professional judgment about risk-adjusted returns across the investable universe—judgment informed by teams of analysts and decades of market experience.

The Rollover Mechanism: Standard Practice, Not Crisis

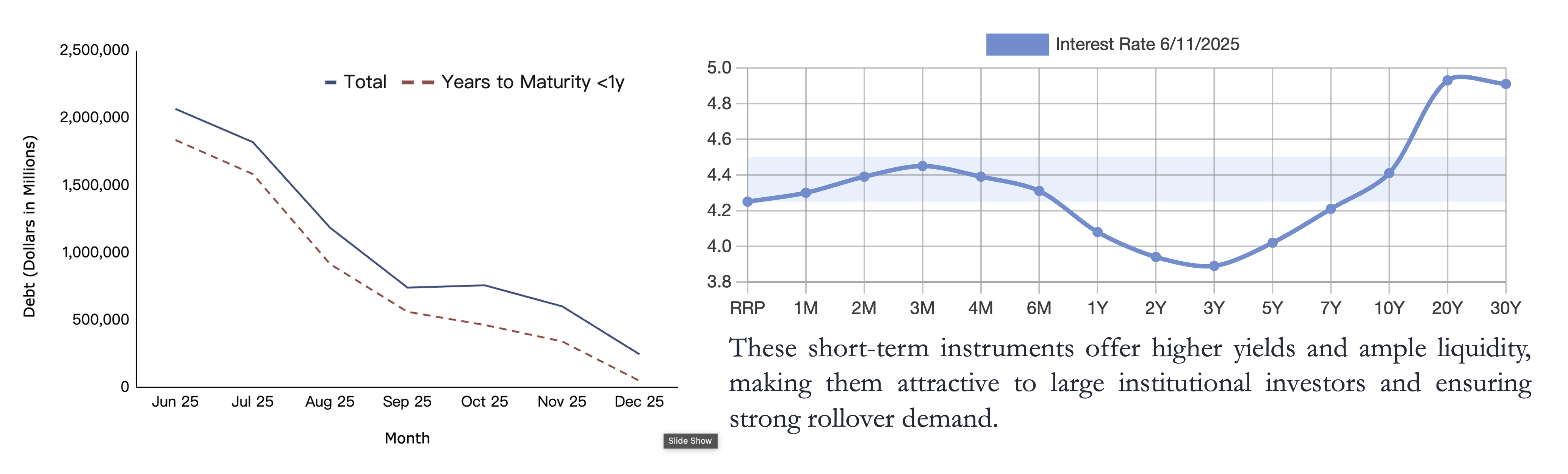

Charts displaying trillions in near-term Treasury maturities circulate regularly with alarming commentary. Yet this presentation mischaracterizes fundamental sovereign debt management practices.

The U.S. Treasury deliberately structures issuance with significant weighting toward short-term instruments. Bills with maturities under one year constitute the majority of outstanding marketable debt. This creates a continuous cycle of issuance and redemption that appears alarming when viewed in isolation but represents intentional design.

Examining maturity schedules across different observation points reveals a consistent pattern: significant maturities always cluster in the near-term window. Whether observed in January, March, or May, the coming months show elevated figures. This reflects issuance structure, not accumulating distress.

Recent data illustrates this dynamic clearly. Maturities in June, July, and August amount to approximately $2.0 trillion, $1.8 trillion, and $1.2 trillion respectively. Instruments with less than one year to maturity comprise between 75% and 90% of these figures. The Treasury routinely refinances these obligations through new issuances—standard practice that maintains market liquidity while ensuring timely debt service.

This short-term structure exists by design. Short-dated instruments offer higher yields and superior liquidity, attracting institutional investors and ensuring robust rollover demand. The mechanism eliminates traditional default risk through systematic refinancing.

Structural Dominance of the Dollar and Treasury Market

Understanding Treasury market dynamics requires appreciating the dollar's foundational role in global finance. The U.S. dollar constitutes approximately 60% of global foreign exchange reserves. International trade settlement, commodity pricing, and cross-border lending overwhelmingly utilize dollar denomination.

This dominance creates structural demand for dollar-denominated assets that persists regardless of yield levels or fiscal headlines. Central banks require dollar reserves for currency intervention and trade facilitation. Global financial institutions need dollar liquidity for operational purposes. The Treasury market represents the only venue capable of absorbing these institutional-scale requirements.

Consider the practical constraints facing large asset allocators. An institution seeking to deploy $100 billion in liquid, low-risk instruments faces limited options. Corporate bond markets lack sufficient scale and introduce credit risk. Other sovereign markets either lack depth or require accepting currency exposure. The Treasury market remains, effectively, the only viable option for institutional-scale safe asset allocation.

Banks require Treasury collateral for regulatory compliance and repurchase agreement operations. Insurance companies need duration-matched assets for liability management. Pension funds require predictable cash flows for benefit payments. These allocations are not discretionary responses to attractive yields but structural requirements driven by regulatory and operational necessities.

The Treasury market's depth and liquidity remain unmatched globally. This creates a self-reinforcing dynamic: institutions need Treasuries because the market can absorb their size, and the market maintains depth because institutions consistently participate.

Federal Reserve Policy Trajectory

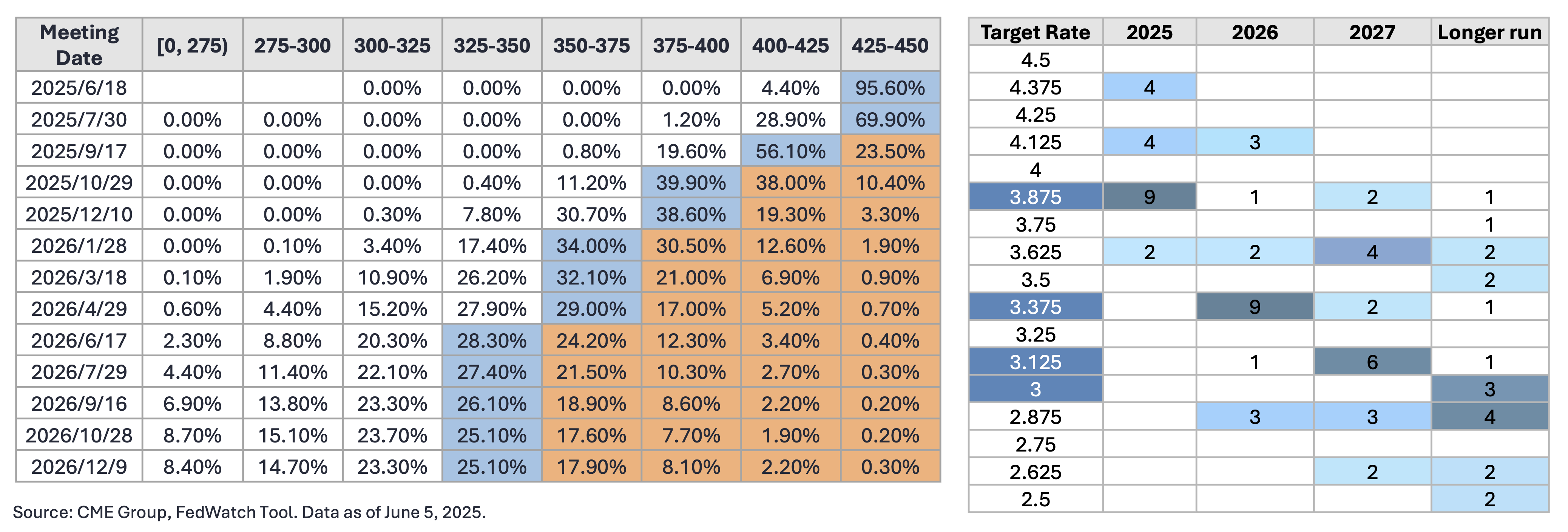

The Federal Reserve's policy stance significantly influences Treasury yields across the maturity spectrum. Following an extended period of restrictive monetary policy aimed at controlling inflation, market expectations have shifted toward eventual easing as inflation moderates and labor market conditions evolve.

Current market pricing, as reflected in federal funds futures, suggests a gradual path toward lower policy rates over coming quarters. While precise timing remains data-dependent, the directional trajectory points toward accommodation.

This prospective shift carries important implications for understanding yield dynamics. Money market instruments and short-term deposits currently offer attractive yields, but face reinvestment risk as policy rates decline. The Federal Reserve's dot plot projections indicate expectations for rates to move progressively lower through 2025 and 2026.

Market participants anticipate this transition, which influences positioning and pricing across the yield curve. Short-term rates closely track Fed policy expectations, while longer-term yields reflect additional factors including inflation expectations and term premiums.

The 10-Year Treasury Yield Outlook

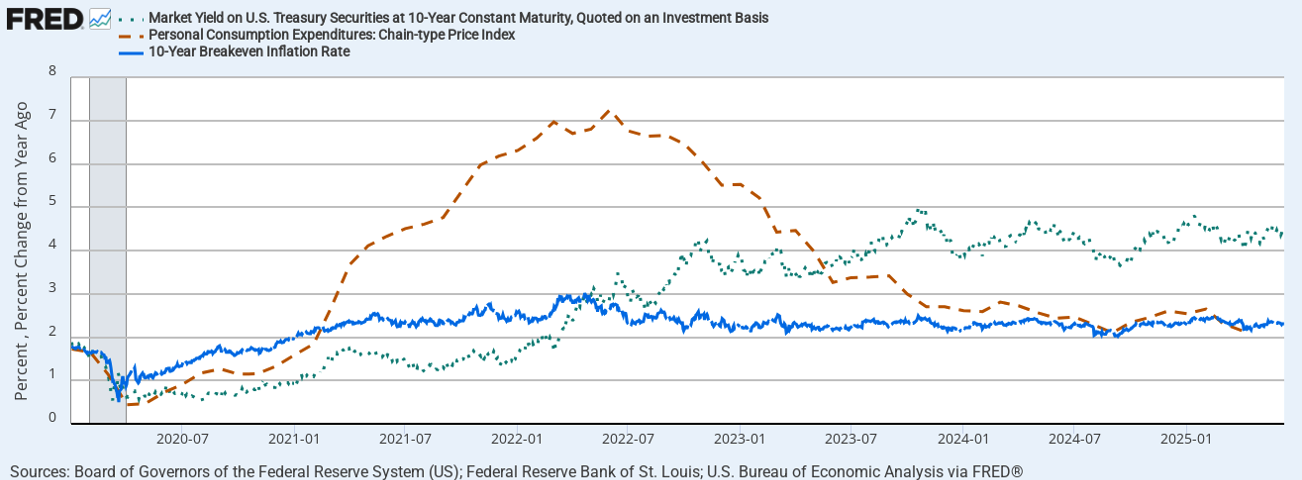

The 10-year Treasury yield serves as a benchmark for mortgage rates, corporate borrowing costs, and countless other financial instruments. Its movements reflect complex interactions between inflation expectations, term premiums, supply dynamics, and policy signals.

Long-term inflation expectations have stabilized as actual inflation has eased from its peak. The 10-year breakeven inflation rate—derived from the spread between nominal Treasuries and inflation-protected securities—provides market-based evidence that long-term inflation concerns have moderated.

Policy discussions have highlighted potential regulatory adjustments that could influence Treasury demand. Proposals to modify the Supplementary Leverage Ratio—which affects how Treasury holdings impact bank capital requirements—could meaningfully increase financial institution demand for government securities. Tax incentive considerations for domestic Treasury investment may further support demand dynamics.

Treasury Secretary Bessent has articulated goals of moderating long-term yields through these regulatory and issuance strategies. While implementation timelines and ultimate impacts remain uncertain, the policy direction suggests supportive measures for the Treasury market.

Current elevated yields on the 10-year note reflect the confluence of factors discussed throughout this analysis: inflation uncertainty, term premium expansion, and supply considerations. For market observers, distinguishing between these drivers and misplaced default concerns remains essential for accurate interpretation.

Conclusion: Clarity Through Proper Framework

The Treasury market in 2025 presents elevated yields, policy transition, and persistent headlines about fiscal sustainability. Navigating this environment requires proper analytical framework—specifically, understanding what yields signal and what they do not.

U.S. sovereign default does not represent a credible scenario given fundamental mechanics of sovereign currency issuance. The relevant questions involve inflation trajectory, Federal Reserve policy response, and term premium evolution. These factors influence market pricing but do not threaten principal repayment.

The Treasury's systematic rollover mechanism, the dollar's structural dominance in global finance, and institutional demand driven by regulatory requirements collectively support market functionality. Observing sophisticated institutional behavior—continued substantial allocations despite headline concerns—provides market-based evidence of this assessment.

For fixed income observers, distinguishing inflation risk from credit risk provides the foundation for accurate market interpretation. Elevated yields reflect legitimate economic considerations about policy direction and inflation expectations. They do not reflect doubts about America's capacity to service its obligations.

Disclaimer: This article is provided for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. The views expressed are those of Medina Partners and are subject to change without notice. Investors should conduct their own due diligence and consult with qualified financial advisors before making investment decisions. Medina Partners and its affiliates may hold positions in securities mentioned herein.